Avoiding geopolitical risk in the Australian agriculture sector

This essay was written as a response to the AgriEducate Essay Writing Competition 2020

Geopolitical risk, but more specifically, trade-based economic coercion from the Chinese Communist Party (CCP) presents as arguably the most considerable risk to the Australian agriculture sector, rivalled only by climate change. Following the ascent of Xi Jinping to power in 2012, the CCP has reaffirmed more authoritarian values, often at odds with liberal democracies.1 Chinese objection on the political scene has since spilled over into trade strategy, leaving every country with a dependence on China heavily exposed to political manipulation. Industries like agriculture and mining are at risk as Australia increases efforts to protect its sovereignty, hold the CCP accountable and upholds its values. To mitigate this risk, governments should focus on long term efforts, including business education, trade partner diversification and political discipline. In the short term, a tit-for-tat trade strategy may be useful in reducing the frequency of the CCP's attempts at political strong-arming but should be avoided if possible due to the destructive nature. Individual farmers also hold responsibility for crop and revenue stream diversification, whilst the Australian insurance market may see some value in a novel political risk insurance product to protect farmers and serve as a new revenue stream. We cannot deny the Australia agriculture sector has left itself exposed due to customer concentration; however, as participants become aware of the risk, a significant reduction is possible.

Contemplating risk within the Australian agricultural sector requires targets. What quantity or progression becomes jeopardised by the realisation of a risk factor? The National Farmer’s Foundation (NFF) is the peak body representing farmers and more broadly agriculture across Australia. The NFF developed a roadmap to exceed farm gate output of $100B by 2030, known simply as the “2030 Roadmap”. This roadmap is widely accepted as the industry target, representing approximately a $40B (67%) increase from where we stand today.2 The $100B figure is also $16B above the predicted output at current trends – meaning there would have to an acceleration of growth on today’s standards. In specific regard to trade, the NFF roadmap seeks to “Champion efforts to open new markets, reduce tariffs and increase quotas for Australian produce”, with the metric measuring this progress listed as “An average tariff faced by agricultural exports of 5%”. The NFF Roadmap also makes specific reference to a goal of a 50% reduction in exports which experience non-tariff barriers. During the development of the 2030 Roadmap, the NFF consulted with 380 industry stakeholders including both private sector and government entities, farmers, researchers, educators and government.

The goals seen in the 2030 Roadmap and projections from the discussion paper feature a key trend which is of significance; they include robust demand from Asia, and incredibly strong demand and growth in demand from China. James Fell from The Australian Bureau of Agricultural and Resource Economics (ABARES) comments, “The rise of food consumption in China will be characterised by a move towards more western-style diets, with higher intake of high-value foods, such as dairy products, beef, sheep and goat meat, fruit and vegetables. Consumption of starchy staples, such as rice, is expected to fall as rising incomes allow households to diversify the foods they consume.”3 A 2014 Report by ABARES titled “What Asia Wants” neatly summarises the general industry consensus:

“In China, sustained income growth is projected to lead to significantly higher demand for many food commodities. Compared with 2007, the real value of consumption in 2050 is projected to rise by 18 per cent for coarse grains (in 2007 US dollars hereafter), 61 per cent for vegetable oil, nearly double for sugar and beef, 75 per cent for sheep and goat meat and more than double for dairy products. Higher domestic consumption is expected to lead to increased import demand for these commodities.”4

These are two examples, but the overarching message within the industry is that China is expected to continue being the heavyweight they are today – and even accelerate growth from here. To be clear, this is no critique of ABARES or the NFF Roadmap. These projections are based on evidence, historical trends and many thousands of hours of in-depth consultation with relevant stakeholders. In all likelihood, the Australian agricultural sector will continue to export a large share of production to China with little deviation from the current path.

There are several conclusions we must draw from this assumption. Firstly, even though the likelihood is that nothing will change – we must consider the situation in which things do change. In what scenario can we no longer rely on a robust Chinese export market? Related to this, but a more worrying implication - if the future of Australian agriculture is China-dominated, then China, but more specifically the CCP, holds a large degree of power in determining the Australian agricultural future.

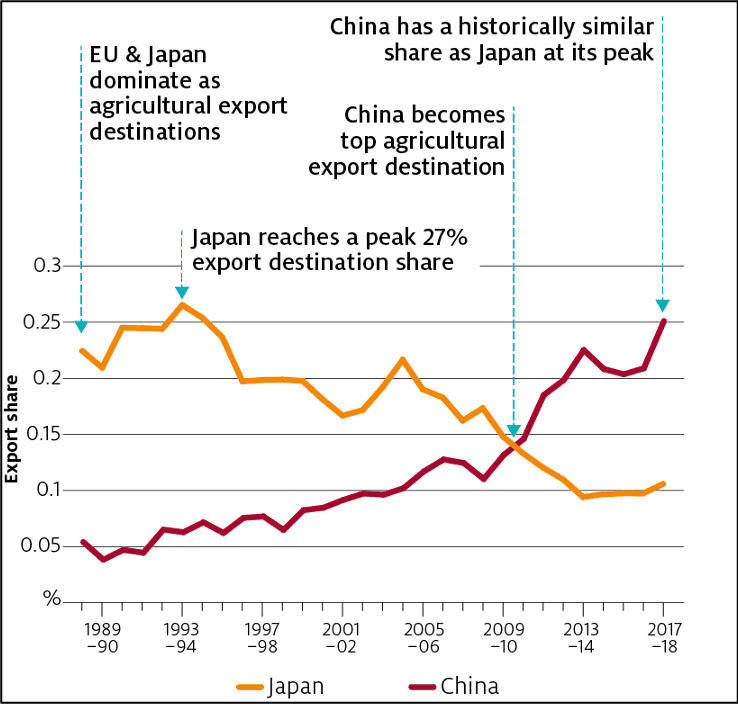

Figure 1 - ABS Export Share China vs Japan (2019). Some figures adjusted for confidentiality

Figure 1 - ABS Export Share China vs Japan (2019). Some figures adjusted for confidentiality

How much power? Of course, this is a difficult question to answer. To get some rough estimates, however, we can consider the role China occupies today. The Rural Bank estimates China accounted for 28.4% of Australian agricultural exports in FY2018-19, with a compound annual growth rate of 15.8% over the last ten years.5 China is also the major exporter for all commodity groups, excluding vegetables, sugar and beef. China is so important to Australian agricultural exports that it accounts for more export value than the next three export markets (USA, Japan and the Middle East/North Africa).

The Department of Foreign Affairs and Trade indicates that around two-thirds of agricultural products produced in Australia are exported, with only 35% on the revenues going to the sector coming from domestic consumers.6

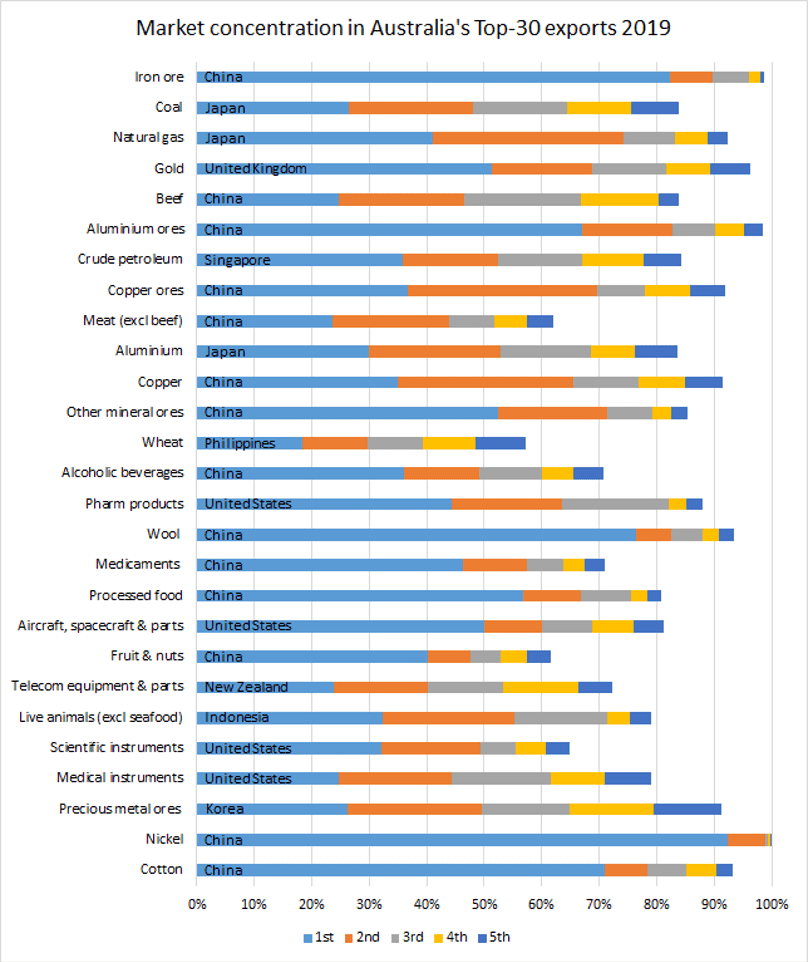

Figure 2 - Perth USAsia Centre submission to the Joint Standing Committee on Foreign Affairs, Defence and Trade Inquiry into the implications of the COVID-19 pandemic

Figure 2 - Perth USAsia Centre submission to the Joint Standing Committee on Foreign Affairs, Defence and Trade Inquiry into the implications of the COVID-19 pandemic

These figures are disconcerting if you are a stakeholder in Australian agriculture and even the Australian economy generally. Export dependence increases the economic risk to exogenous shocks, and the magnitude of that risk is strongly correlated to export concentration.7 Whilst exogenous shocks present a threat, this does not even consider a more pressing issue at the heart of the matter: China relies heavily on trade-based economic coercion to further the diplomatic goals of the CCP.

As China's industrial dominance has grown since the early 2000s, the CCP has increasingly relied upon economic means to punish countries and businesses that cross Chinese interests on sensitive issues. In an article published in the Quarterly Essay, Peter Hartcher details at least 11 examples of the CCP imposing specific trade tariffs for transgressions of Chinese interests from trading partners in the last ten years.8 These transgressions include wide-ranging political matters such as territorial disputes, support for dissidents, support for democracy in Hong Kong/Taiwan and even the installation of US missile defence systems by regional neighbours. A key characteristic of this approach is that the CCP likes to have plausible deniability, and often targets particular industries citing some disruption to trade utilising the complex WTO laws. As the Lowy Institute writes, “Rather than publicly announcing formal legal sanctions and linking them to a foreign policy dispute, Beijing typically denies that it is imposing economic punishments while explaining the disruption to trade by reference to other plausible justifications.9 The China-US trade war was not included in Hartcher’s analysis, but the tit-for-tat tariff war gives us an indication of how quickly tariffs can negatively affect an industry. The US agricultural sector saw exports to fall from $15.8B to $5.9B between 2017 and 2018.10

Australia has begun to feel the might of Chinese economic power following the Morrison government’s stance on several issues; Banning Huawei from the 5G network, speaking up about human rights abuses in Xinjiang and advocacy of an international inquiry into the origins of coronavirus. The Chinese Ambassador to Australia, Cheng Jingye, denounced the Australian government's involvement (into the coronavirus probe) as "dangerous" and politically motivated. The Ambassador further added that Chinese consumers might lose their taste for Australian beef and wine.11 Following this interview with the Australian Financial Review, China imposed 80.5% tariffs on Australian barley, much higher than the expected 56.14% following the anti-dumping investigation initiated in 2018.12 Alongside this, China also banned four major abattoirs from trade, citing labelling issues, and another for chemical detection.13 An anonymous beef analyst from China noted that the latest ban was politically motivated:

“This announcement is partly related to the current difficult China-Australia relationship… China Customs destroyed the whole batch of goods and it will have a strong psychological impact to Australian beef traders. They will shy away from Australia suppliers and increase beef import from other regions… To be honest, I’ve warned my friends in the beef-importing business not to touch Australian beef this year. It is extremely risky due to the frosty China-Australia relationship.”14

China also followed through with its threat on wine, launching an anti-dumping probe into Australian exports of wine and one week later another countervailing-duties investigation into containers less than 2 litres. Dr Jeffrey Wilson from the Perth USAsia Centre commented in an interview with the ABC “China's probe against Australian wine follows the same logic as recent moves against barley — the use of seemingly 'technical' trade measures to disguise what is fundamentally a political sanction”.15 More recently, China also announced it would apply enhanced inspections on shipments of wheat arriving in Australia.16 As tensions cool further, these types of measures will become the norm. Another factor to consider is Australia's close relationship with the US. Australia-US allegiance will become a key talking point as China moves into superpower status. We can easily find more examples of such behaviour from the CCP. The question then becomes, how exactly can we protect Australian farmers against such political risk?

On a macro level, an effective strategy would need to include Federal government policy to circumvent the 'economic coercion' from the CCP mentioned above, whilst simultaneously preserving economic prosperity in Australia. Pathways in this direction are numerous; however, we will consider how the Australian government can utilise game theory to guide economic policy regarding the CCP. In 2018 the Chinese economy was 9.4 times the size of the Australian economy17, and Chinese exports accounted for 6.7% of Australian GDP.18 In the same period Australia only accounted for 1.9% of China’s exports.19 You may then ask the question; if Australia has such power relative to China, how can we model interactions using game theory which depends on relatively equal power. A possible answer lies in China's reliance on Australian iron ore. In 2019, China imported a staggering 62% of its iron ore from Australia, almost three times as much as the second closest competitor, Brazil, with 21%.19 Foreign affairs analyst Darren Lim from the Australian National University commented on the hesitation of the CCP to implement sanctions that may affect the production side. "They view the political costs of such disruption (in terms of job losses and ripple effects) to be too great”.20 As with any trade flow, involving iron ore in a dispute will cut both ways. Australia exports 90% of its iron ore to China21, and iron ore accounts for around 30% of Australian exports.22 Iron ore is the nuclear option – Australia should avoid using it if possible, not to mention that it would be highly unusual Australia to engage in such a policy.

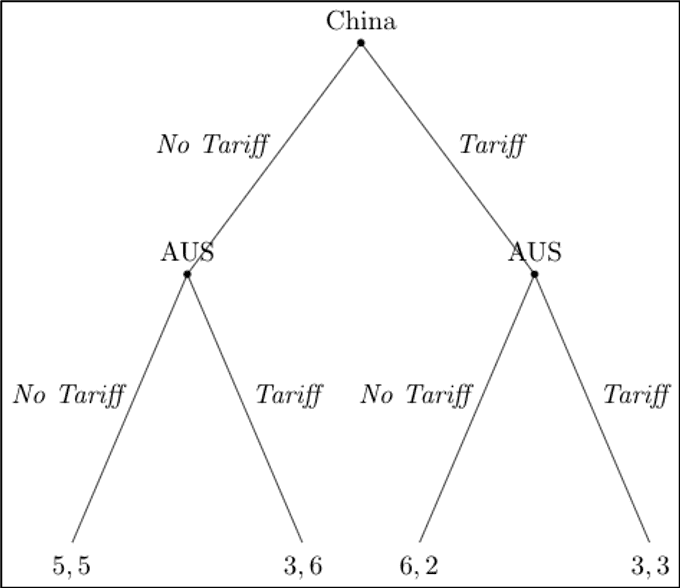

Game theory allows us to model how using export restrictions on China will play out. Consider a 2-move game, in which China moves first. This game is a highly simplified model but allows us to think about how the Australian government should respond to Chinese actions and the relative payoff of different responses. This sort of model is especially crucial in the short term, where other reform measures such as diversification and subsidies for agriculture are out of scope. Note, in considering the binary reality of “Tariff” vs “No Tariff”, the tariffs here represent relatively equivalent quantities. E.g. an 80% tariff on Australian barley could be met with a +30% increase on import duty for manufactured steel from China, both with relatively equal monetary effects.

We can see here from the respective payoff values (China,Australia), that having open trading policies is in the best interests of both partners. When there are two-way tariffs, this does not particularly benefit anyone. The propensity of China to impose tariffs as the aggressor means that Australia is likely to be faced with the right-hand scenario. In this situation, it may be of value to impose a tariff or trade restriction on China. As we have seen with the US-China trade war; however, this sort of tit-for-tat style of trade negotiations leads to both parties being worse off. The ultimate goal of such a strategy is short-term destruction, leading to more cooperative policy in the longer term. If Australia places a trade restriction on iron ore, it will hurt the CCP politically and force them to reconsider utilising economic means to assert foreign policy objectives.

Conversely, would be an incredibly unpopular domestic policy considering the relative value of iron ore exports. In the short term, this is one of the very few options available to the Australian government apart from conceding to the whims of the CCP, or doing nothing at all and suffering the losses induced by tariffs. It is worth noting that such losses may direct the market towards alternative trade partners - a desirable outcome. We can conclude that although there is merit in dealing with Chinese coercion using a tit-for-tat strategy, using it is a last resort.

On a longer timeframe, we can suggest some slightly more preferable strategies for dealing with the economic coercion of China, but there will be no easy options. As Sam Roggeveen from the Lowy Institute writes, “The word ‘diversification’ trips far too easily off the tongues of Australian strategic commentators.”23 Consider the dollar value of exports going to China, estimated at $12.3B in FY2018-19.24 To make a meaningful divergence or 'diversification' to say only 20% of Australia's agricultural exports (currently ~ 30%) would require finding a new market for $4B worth of exports. That's equivalent to the value of Australian agricultural exports to the USA. Long term diversification will take time and require sustained efforts. Australia has begun to take steps to build better trading relationships with other partners, including hosting the ASEAN summit in 2018, the Indian Economic Strategy25 and working on expanding Australia's free trade network. In February 2020 parliament also begun an Inquiry into Diversifying Australia's Trade and Investment Profile.26 Some other ideas the government could implement in the short run include:

- The Morrison government needs to operate with discipline regarding China. No unnecessary provocation but also not caving to their impositions on sovereignty

- Ensure the businesses sector has the necessary information to deal with the risks that dealing with China entails, including trade disruptions, cyber risk, manipulation and intimidation

- Provide more resources through DFAT and other organisations to help businesses diversify output, diversify buyers and encourage long term thinking.

The goal here is to reduce the volatility induced by trade issues on Australian farmers. Volatility makes conducting business in any form difficult and reduces the likelihood of long-term survival. ABARES included a thought-provoking section on their 2020 Snapshot of Agriculture, indicating the high levels of risk faced by Australian farmers. The report suggests Australian farmers face the highest natural and economic volatility out of the 15 countries surveyed.27 The last resort for the government will be to give high levels of subsidies to Australian farmers. Subsidies are always tricky, become highly contentious and if possible, should be avoided.

Individual operators in the agricultural value chain similarly hold a responsibility to mitigate China-specific risk. Farmers should consider buyers in other countries, even if at slightly lower prices. A report by ABARES notes a significant possibility for export growth in India, with “Income growth, population growth and urbanisation are projected to underpin large increases in agri-food consumption in the future”. The report also concludes that “Dairy products, fruit and vegetables will be those commodities most strongly in demand by 2050” as agricultural consumption will double by 2050.28 Of course, there are significant challenges associated with entering a new market. India has relatively closed agricultural markets and doesn't lend itself towards imports/exports trade like China. Market barriers present enormous obstacles for entering both the EU and Indonesia, and higher levels of effort into free trade agreements will be required to enter these markets.29 That being said, Australia likely has a China problem because Australia has always focused on China. If the rest of the world gets more attention, the likelihood for increased access and potential earnings increases significantly. Farmers could also consider alternative lines of revenues – such as biofuels or carbon capture and sequestration. The Emissions Reduction Fund run by the Clean Energy Regulator is an example of a pathway to achieve this.30 The ERF offers Australian carbon credit units for negative emissions entities, providing payment for carbon sequestered. Farmers will need to address these issues on a case by case basis; however, the message is clear - there is an inherent risk in having a customer concentration with China.

One last point worth considering revolves around easily the most effective means society deals with uncertainty: insurance. Most major insurers offer some form of political risk insurance today31,32, but these policies are mostly cover for war, civil unrest or embargoes. Agricultural insurance is also usually focused on natural events; even Multi-Peril crop insurance does not include such a risk. Therein lies a unique opportunity for insurance companies in Australia to work directly with farmers to ensure there is some form of financial cover for trade-related losses. Generally, crop insurance is complicated due to the highly specific nature of a given farm, their farming practices and the information available to the insurance company. Trade-related insurance would be quite generic and could be utilised as a once-off payout that gives farmers time to reconsider their options, or possibly diverge away from trade affected crops. Insurers could also assess geopolitical risk on an annual basis and give farmers an indication of the expected premiums for different produce, allowing farmers to understand the risk more effectively. An insurance market will also help to discourage the concentration of trading partners as premiums go up, increasing market efficiency as capital flows follow the inverse of risk (premiums).

The Australian agricultural industry and government must realise the exceptional risk brought on by extensive trade with a trading partner that is willing to manipulate. Such risk is unpredictable and leaves us open as a nation to a compromise on our values, something that is unthinkable for most Australians. These risks need to be dealt with to ensure the long-term prosperity of the agricultural industry.

Footnotes

1. Xi Jinping Thought. (2020). Retrieved 20 September 2020, from https://en.wikipedia.org/wiki/Xi_Jinping_Thought 2030 Roadmap

2. AustralianFarmers. (2020). Retrieved 20 September 2020, from https://farmers.org.au/roadmap/

3. The future of Chinese agricultural policy - Department of Agriculture. (2020). Agriculture.Gov.Au. https://bit.ly/33GVrBy

4. What Asia wants Long-term food consumption trends in Asia. (2013). https://bit.ly/2FSnGVE

5. Australian Agricultural Trade. (2018). https://bit.ly/3kxPde1

6. Agricultural trade | DFAT. (2018). Dfat.Gov.Au. https://bit.ly/2REG4UK

7. Towards Human Resilience: Sustaining MDG Progress in an Age of Economic Uncertainty | UNDP. (2015). UNDP. https://bit.ly/2He1eqF

8. Red Flag. Quarterly Essay. https://www.quarterlyessay.com.au/essay/2019/11/red-flag

9. Lim, D. (2020, May 12). In beef over barley, Chinese economic coercion cuts against the grain. Lowyinstitute.Org; The Interpreter. https://www.lowyinstitute.org/the-interpreter/barney-over-beef-chinese-economic-coercion-cuts-against-grain

10. PBS NewsHour. (2020, January 16). What is the toll of trade wars on U.S. agriculture? PBS NewsHour. https://www.pbs.org/newshour/economy/making-sense/what-is-the-toll-of-trade-wars-on-u-s-agriculture

11. Tillett, A. (2020, April 27). Payne lashes China’s “economic coercion.” Australian Financial Review; Australian Financial Review. https://www.afr.com/politics/federal/payne-lashes-china-s-economic-coercion-20200427-p54nja

12. Weihuan Zhou. (2020, May 23). Rethinking economic coercion as Australia–China relations fracture | East Asia Forum. East Asia Forum. https://bit.ly/3kKN4fp

13. Australian abattoirs still suspended from trade with China as labelling concerns addressed - ABC News. (2020, June 12). ABC News. https://www.abc.net.au/news/rural/2020-06-12/abattoirs-still-suspended-from-trading-with-china/12349732

14. Smith, M. (2020, August 28). China slaps new ban on Aussie beef. Australian Financial Review; Australian Financial Review. https://www.afr.com/companies/agriculture/china-slaps-new-ban-on-aussie-beef-20200828-p55q5x

15. China launches anti-dumping investigation into Australian wine exports - ABC News. (2020, August 18). ABC News. https://www.abc.net.au/news/2020-08-18/china-launches-investigation-into-australian-wine-exports/12569640

16. China puts Australia on notice over wheat exports - ABC News. (2020, September 14). ABC News. https://www.abc.net.au/news/rural/2020-09-14/china-put-australia-on-notice-over-wheat-exports/12661710

17. Countryeconomy. (2020). Country comparison Australia vs China 2020. Countryeconomy.Com. https://bit.ly/3kzgX28

18. Australia-China trade stoush over coronavirus inquiry puts exports — and more —at risk - ABC News. (2020, May 15). ABC News. https://www.abc.net.au/news/2020-05-15/australia-china-trade-stoush-over-coronavirus-inquiry/12241640

19. China Exports By Country and Region 2018. (2018). Worldbank.Org. https://bit.ly/2EicbGL

20. Fowler, E. (2020, May 14). Why China needs Australian iron ore. Australian Financial Review; Australian Financial Review. https://www.afr.com/companies/mining/why-china-needs-australian-iron-ore-20200514-p54sts

21. Fickling, D. (2020, September 12). Australia Has a Nuclear Option in Its China Diplomacy. Bloomberg.Com; Bloomberg. https://www.bloomberg.com/opinion/articles/2020-09-12/australia-china-diplomacy-economic-ties-come-down-to-iron-ore

22. Salomae Haselgrove. (2020, July 27). Iron ore becomes Australia’s $100bn export industry - Australian Mining. Australian Mining. https://www.australianmining.com.au/news/iron-ore-exceeds-100bn-in-export-value/

23. Roggeveen, S. (2020, July 15). Canberra vs Beijing: Getting serious about costs. Lowyinstitute.Org; The Interpreter. https://www.lowyinstitute.org/the-interpreter/canberra-vs-beijing-getting-serious-about-costs

24. Overview of recent ABARES China research - Department of Agriculture. (2014). Agriculture.Gov.Au. https://www.agriculture.gov.au/abares/research-topics/trade/overview-recent-china-research#events-in-china-affect-australian-farmers

25. An India Economic Strategy To 2035 - Department of Foreign Affairs and Trade. (2018). Dfat.Gov.Au. https://www.dfat.gov.au/geo/india/ies/index.html

26. Inquiry into Diversifying Australia’s Trade and Investment Profile – Parliament of Australia. (2020). Aph.Gov.Au. https://bit.ly/3kyXlel

27. Snapshot of Australian Agriculture 2020 - Department of Agriculture. (2020). Agriculture.Gov.Au. https://bit.ly/2RInMBY

28. Analysis of opportunities in India - Department of Agriculture. (2020). Agriculture.Gov.Au. https://bit.ly/3hN9gn4

29. Diversification: trade mission impossible? (2020). Anz.Com. https://bit.ly/3hMe4Jr

30. Step 4-Delivery and payment. (2020). Cleanenergyregulator.Gov.Au. http://www.cleanenergyregulator.gov.au/ERF/Want-to-participate-in-the-Emissions-Reduction-Fund/Step-4-Delivery-and-payment

31. Political Risk - Insurance from AIG in Australia. (2020). Aig.Com.Au. https://www.aig.com.au/business/products/political-risk

32. Political Risk Insurance | Aon. (2020). Aon.Com. https://www.aon.com/middle-east/risk-solutions/political-risk-insurance.jsp

![]()